Buying a Portfolio of Properties.

Disclaimer: this article is not financial advice and should not be treated as such. It is a discussion based on personal circumstances and preferences and so should not be generalized to other situations without careful thought.

As shown in my previous post here, buying a property to rent out in Liverpool can be a good investment option. However, one property is not enough to retire on, so the next step is to see how this idea scales and evolves over time. The portfolio will be owned by a limited company to benefit from treating interest payments as tax deductible costs. While this is not the right choice for everyone, my own personal circumstances mean it is better for me. In my last article I looked at return-on-investment as the key metric to compare investments. However, my primary aim was to retire. This means extractable cash flow is a better metric to evaluate the success of a business venture as this can be used as a passive income stream. My goal is to have an income of around £3000 per month (pre-tax), but obviously the more the better.

This investigation will look into how the cash flow from a property portfolio evolves with time as more money is invested into the project. Three scenarios are considered.

- That £20,000 can be invested into the company every six months for the first three years of the company which is used to purchase properties. Housing can be purchased only during the first three years.

- That £40,000 can be invested into the company every six months for the first three years of the company which is used to purchase properties. Housing can be purchased only during the first three years.

- That £40,000 can be invested into the company every six months for the first three years of the company which is used to purchase properties. Housing can be purchased during the first five years of the company.

1) Modelling the Business

In my previous post I used the price of £150,000 per house and a rental income of roughly £17,000 per year. While there are plenty of examples of properties with these numbers, to be conservative this model will assume each house costs £160,000 and rental income is £15,000. This is to account for the property market becoming more competitive with time either due to competition or our own market impact. Inflation will not be accounted for in this model as it is assumed income will scale with costs.

This model works by breaking the company down into four components, each representing a higher level of

abstraction: housing, management of the housing portfolio, the external funding and the investment decision

making part based on the input from the external funding and housing portfolio. Each house is treated as an

independent object with its own associated cost schedule and income which was described in my original blog post. The management piece takes collective action based on the cost schedule of its constituent houses. The external funding just adds money to the accounts that can be used to purchase more houses. The top level investment decision making part looks at the money available in the accounts to decide if the model has sufficient money to purchase another house.

An important part of this investigation is correctly modelling cash flow. In the original post we deducted the average cost of repairs each month to calculate the profit. In real life this money will need to sit somewhere and then be used to pay bills as they come up. If bills come close together then they may cost more than the company has saved. Equally, having multiple properties may mean there is enough income to cover bills on an ad-hoc basis and more money can be extracted from the company. This is discussed next.

- Modelling of the Housing Portfolio

The housing portfolio part of the model is where the aggregated cash flow of all the houses is managed. It models the saving of money for maintenance and decides when to let money leave the housing portfolio to either be reinvested into more properties.

Any property is assumed to be in perfect condition after initial repairs are done at time of purchase. This assumption may be a generous one, but the conservative price the model assumes for the house smooths out this assumption.

After paying percentage based costs, such as property management fees, the rent is split into a part which can be extracted from the housing unit and one that is saved to cover future expenses. In the model there are two values considered when saving:

i) a minimum cash amount in the account to handle the maintenance costs and

ii) an additional amount of money stored per house as a contingency fund to make sure the company can always pay the bills.

Any money above the minimum cash amount is assumed to be stored in liquid assets yielding a 4% return. If the amount of money saved is equal to the desired saved amount than any additional income can be extracted from the housing portfolio. For example, if the portfolio has two houses, a minimum cash reserve of £10,000 and a per house reserve of £1,500, and the saved amount is £13,000, then any money that would be saved for future repairs above this amount can be extracted and re-invested. Repairs and maintenance are done according to the repair schedule described in the original article. Thus, every seven years after the house purchase a new kitchen will be bought for the property; estate agent fees will be paid every year. Costs associated with mortgages are paid every three years to remortgage the property. Money is first deducted from the cash reserve and then from the invested reserve. At the end of each month if the cash reserve is ever below the minimum amount money is transferred from the invested reserve if possible.

1.2 External Funding

This income stream represents invested money from the owners of the company. It assumes every six months an amount is invested into the company. In all scenarios investigated, this investment is assumed to carry on for three years to account for the investment horizon of this project.

1.3 Combined Business

The housing portfolio and external funding are treated as separate business units and every month the combined business extracts whatever money the business unit allows. The model will then purchase as many properties as allowed by its bank balance each month. Money extracted from the housing portfolio is taxed at a rate of 19% which is paid once a year in April. The company makes sure to keep enough money in reserve to pay tax. This reserve is an inefficient use of capital and can probably be improved. However, as the sums involved are small compared to the cost of a property this is likely to be a minor effect for this investigation.

2 Model Results

Before diving into the different business scenarios, it is worth looking at a single house again as some starting assumptions have changed since the last article. The cost of investing in a single property is £50,500 and the annual extractable income from it is £5,000. This works out to be a levered return of about 10% per annum. This is still a very promising starting point.

As described in the introduction, each scenario has different starting parameters. However, one common parameter across all scenarios is an initial bank balance of £35,000 so a house can be purchased after the first batch of external funding. Minimum cash and per house reserves are chosen such that the company does not go bankrupt over 30 years of projected maintenance. The business will be evaluated by its performance over the first 5 years with the assumption that it starts on 1st January 2020.

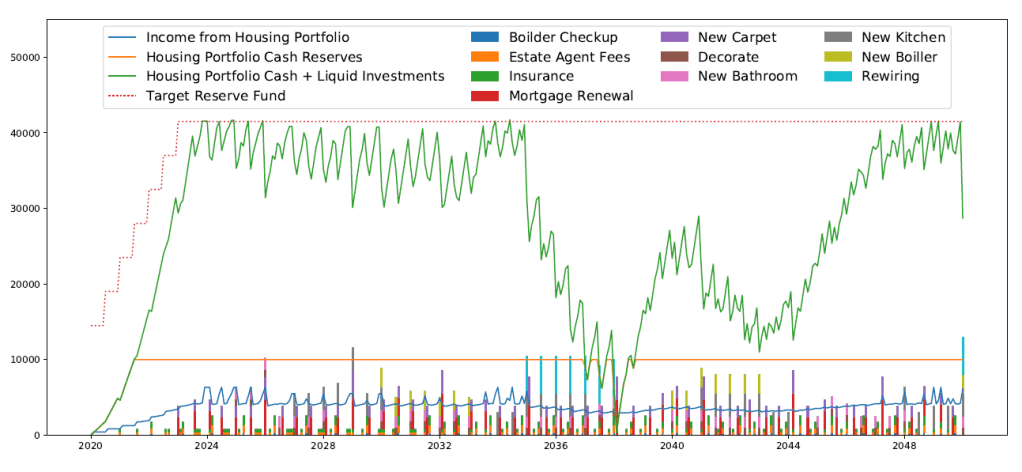

2.1 Scenario 1

In scenario 1 £20,000 will be invested every six months for the first three years and houses are purchased for the first three years. The minimum cash reserve is £10,000 and the per house reserve is £3,500. Table 1 shows a summary of the business under scenario 1 for the first 5 years. Figure 1 shows a thirty year projection to give an idea of the full cash flow cycle. It can be seen that the reserve amount is driven by cash flow around 2035 when rewiring work is needed on the properties.

The average monthly income is derived from the cumulative income over the year divided by 12, so to smooth out any month-by-month fluctuations. These fluctuations are caused by the nature of the income stream. The rent component roughly stable, but cash can be extracted when the saving target has already reached and from returns on the invested fraction of the cash reserve. A large bill can reduce the saved reserve enough that it takes months to recover and hence the extractable money is reduced. An important point under this scenario is that cash from the invested reserve and not saving above our reserve amount contributes a significant amount to total cashflow. In year 5 the average income from 3 houses purely from rent is around £1,200 but the average income is £2,000.

Table 1: Summary of the business under scenario 1.

| Year | Average Monthly Income [£] | Number of Houses |

| 2020 | 400 | 1 |

| 2021 | 600 | 2 |

| 2022 | 1100 | 3 |

| 2023 | 1500 | 3 |

| 2024 | 2000 | 3 |

Figure 1: 30 year projection of business cash flow for scenario 1.

2.2 Scenario 2

In scenario 2 £40,000 will be invested every six months for the first three years and houses are purchased for the first three years. The minimum cash reserve is £10,000 and the reserve per house is £4,000. Table 2 shows a summary of the business under scenario 2 for the first 5 years. Figure 2 shows a thirty year projection to give an idea of the full cash flow cycle. Doubling the investment results in more than doubling the monthly income. This is because the portfolio starts to generate enough money on its own to purchase new properties. However, the external investment still dominates the available income for the business over the period that is being looked at.

Table 2: Summary of the business under scenario 2.

| Year | Average Monthly Income [£] | Number of Houses |

| 2020 | 560 | 2 |

| 2021 | 1500 | 4 |

| 2022 | 2800 | 6 |

| 2023 | 4200 | 7 |

| 2024 | 5200 | 7 |

Figure 2: A 30 year projection of cash flow in Scenario 2

2.3 Scenario 3

In scenario 3 £40,000 will be invested every six months for the first three years and houses are purchased for the first five years. In this scenario, the minimum cash reserve is £10,000 and the reserve per house is £2,000. Table 3 shows a summary of the business under scenario 3 for the first 6 years. Figure 3 shows a thirty year projection to give an idea of the full cash ow cycle. The per house reserve value is lower than in scenario 1 and 2 as the monthly maintenance contribution from the larger number of houses can offset more of the repair costs. Despite having more houses, the monthly income after 5 years does not increase by much. This is because in scenario 2 money could be returned to investors when the saving threshold was met around 2023. In scenario 3 the saving threshold is not met until after 2024.

Table 3: Summary of the business under scenario 3

| Year | Average Monthly Income [£] | Number of Houses |

| 2020 | 550 | 2 |

| 2021 | 1450 | 4 |

| 2022 | 3400 | 6 |

| 2023 | 4300 | 8 |

| 2024 | 5250 | 9 |

| 2025 | 5550 | 9 |

Figure 3: A 30 year projection of cash flow under scenario 3.

3 Summary

Our current models suggest that the idea of purchasing houses to produce a stable income is a viable one. However, only scenario 2 and 3 produce an income which a single investor could live. The similar income in scenario 2 and 3 suggest scenario 2 is the minimum viable scenario to meet my aim of retiring early and will also let me do so the quickest. However, waiting two more years before stopping reinvestment would allow the company to function on a much lower reserve amount and the higher number of houses in model means the stable rent component of the income stream will be larger.

One area this model does not cover is the effect of interest rate changes. It assumes a low interest regime at least for the next 5 years. Any increase to interest rates would reduce the profitability of this project as cash would need to be directed to pay off debt and to cover increased costs of servicing the existing debt.

One thought on “Housing as a Portfolio”