Disclaimer: this article is not financial advice and should not be treated as such. It is a discussion based on personal circumstances and preferences and so should not be generalized to other situations without careful thought.

In my previous posts (here and here) I looked at buying a house to rent in Liverpool. I chose Liverpool based upon some brief research on Zoopla. I picked a handful of UK cities, and searched for two bedroom flats near the city center for sale and rent. Based on these figures I calculated a rough rental yield and Liverpool was seen to be the best. However, this was a very rough piece of research which left a lot of room for improvement. Making use of freely available data on the internet I should be able to improve this search to look at all cities within the UK to make sure I do not miss any opportunities.

Collecting the Data

House Prices – The UK land registry is a very useful resource for this data. This website provides the address and price of all properties sold in the UK. The geographical coordinates of the property can be derived from the address.

Post Code Geographical Coordinates. – To convert the addresses from the house price data to geographical coordinates I used their post code. Thanks to this website a complete list of postcodes and their coordinates is freely available. The post-code data comes with longitude and latitude. To make it easier to plot the data and compare locations I converted these coordinates to the same system used by OpenMaps .

City Locations – The final piece of the puzzle is the geographical location of cities in Britain. I found a full list of cities here.

Double Checking the Data.

Caution should be applied when dealing with any new dataset, as there is a chance that there is bad data in there. However, for datasets as large as these I would struggle to ensure they are 100% correct as I have nothing to validate them against. However, I can run a few spot checks. For example, I made sure my house purchase was in the pricing data. Using the contextily python module I can link to the OpenMap servers and plots maps for a given location. I used this to spot check that the coordinates I have for the city locations correspond to a city center and I double checked my house’s location showed up in the right spot. This gave me enough confidence to use the data for research.

Results

We now know the location of every sold property and its price. This allows us to do deep lives into different regions. Figure 1 shows a contour map of house prices in Liverpool. We can clearly see just see the expensive area in the city center and that houses are expensive just around the university. We can also use this data to answer our original question, which is the most promising city to invest in. Using the geographical location of each city the average price of all flats within a 4km square of the city center was calculated. Rental data for two bedroom flats near the city center was collected for the cheapest 20 cities. Table 1 shows the 10 cities with the best annual rental income to house price yield. Liverpool is ranked at number 8 in this list, which shows the initial research was not bad. This list is dominated by smaller cities in the north with Bradford at the top of the list. One thing this research does not answer is why Bradford gives such a high yield. There may be many reasons for this, such as a very illiquid market or other market inefficiencies. An in-person trip to the area would be needed to get a full idea of if it’s worth investing somewhere, but this analysis helps narrow down the entire UK into a select list of locations.

Conclusions

This research show there is a large amount of free data online that can be used to inform property investment decisions. Investment approaches can be tested and a list of the best opportunities can be found. Here a list of the best city to buy two bedroom flats based on rental yields was found. To narrow down the list to the final location to buy properties more detailed analysis is needed, but this gives a much better place to start than a manual search.

This article explores using statistical methods to simulate a sales team. From the sales team simulation a set of `historical’ training data is created to fit model which can predict the value of any sales prospects which have not been closed. The predictions are provided as a band giving the upper and lower revenue estimate to a 95% confidence interval. This research acts as a proof of principle that such techniques are be able to be to provide useful information to sales managers.

1 Introduction

A friend of mine manages a sales team. He takes a very analytical approach to the sales process, but has often mentioned the lack of tools available for his projections. This surprised me, as the firm lives or dies based off the performance of its sales team. This article investigates modelling the sales process and the feasibility of predicting future income. The entire sales process is a messy system with lots of moving parts. To make the problem solvable it needs to be broken down into parts. This article focuses on valuing a set of sales prospects, or `pipeline’, at a given point in future based upon historical performance.

2 Terminology

This article is designed to be read by both data scientists and sales managers. There will be many people outside the overlap in the proverbial Venn diagram so I will go over some terminology first.

Throughout this paper the terms `sales prospect’ and `deal’ are used interchangeably to describe the process through which a salesperson first contacts a client and eventually sells something to them. If the salesperson sells the client something then the deal is considered to be closed successfully and failed otherwise.

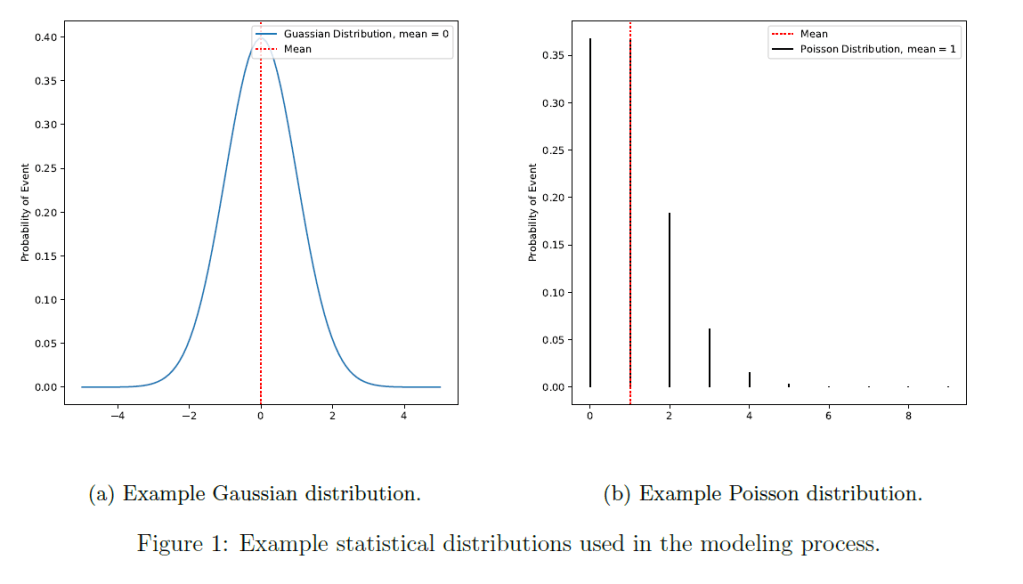

In this article there are many references to statistical distributions with particular focus paid to Gaussian and Poisson distributions, which are shown in figure 1. As a rule of thumb, Gaussian distributions describe situations with continuous values around some average, e.g. a person’s height, and Poisson distributions describe something that occurs only a few times, e.g. the number of goals scored in a football match. For example, it is assumed that the value of a salesperson’s deal follows a Gaussian distribution with an average value and fixed spread (standard deviation). To model future deals a value is selected with the probability that follows a Gaussian distribution, i.e. values that are closer to the average are more likely than those which are far away. This is method is referred to in this article as applying a Gaussian smearing to an expected value.

3 Generating Historical Sales Data

A company’s sales history is confidential information and is not publicly available. As such, this research generates its own data to test ideas by modelling a sales team. The lack of real data will necessarily reduce the applicability of the results but will allow the concepts to be explored. The model has two sets of entities in it:

salespersons which have a set of qualities corresponding with generating sales prospects and

sales prospects which have features based on the generating salesperson but act independently.

3.1 Sales Prospects

The information about a sales prospect that companies record vary between businesses. This is because the database of historical sales can be used in many ways, with each needing a different set of data. However, a common use case in all businesses is for review by a sales manager. As such, each sales prospect needs to keep track of the following features:

The date when the sales prospect is first input into the system.

The date when the sales prospect concludes.

The initial estimate of the sale prospect’s value.

The final value of the sales prospect.

The discount applied on the deal.

These top-level data are used by management to evaluate sales performance. To model a sale, extra pieces of information are required to determine the behaviour of the deal. There are three key modelling variables, the expected deal length, chance of it failing and the difference between the opening price and the closing price.

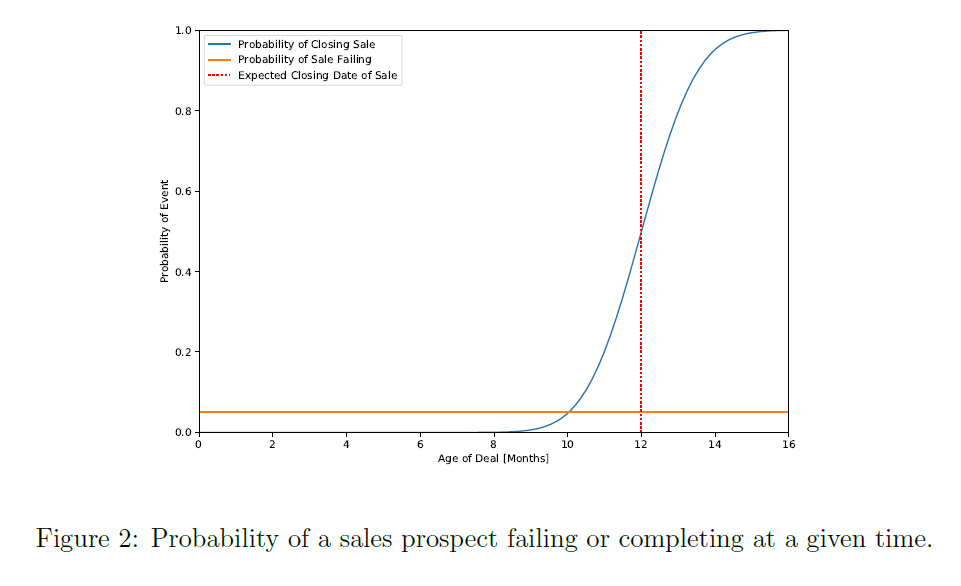

Figure 2 shows how the failure rate and closing time is modelled, where the probabilities of the sale either closing or failing at a given time are shown. The failure rate for a given time is constant, e.g. a sales prospect has the same chance of failing between any two time intervals as any other. The probability of closing a sale is modelled as an expected close date with a Gaussian smearing, where the chance of completion tends to one as the deal moves past its expected close date. If a sale prospect successfully closes, then the final value is decided by the opening value multiplied some Gaussian smeared discount factor. This final smearing accounts for two affects, the change in deal value throughout its lifetime and discount applied to make the sale. These modelling variables are all provided by the salesperson who creates the sales prospect.

3.2 Salespeople

A salesperson is responsible for generating new sales prospects and setting their characteristics based on the abilities of the salesperson. In this model, a salesperson has the following characteristics:

average deal length,

deal length uncertainty,

deal failure rate,

average deal value,

deal value uncertainty,

average discount,

discount uncertainty and

deals generated per month.

Each month a salesperson generates a number of new sales prospects based upon a Poisson distribution of the expected number of deals. Each deal has an opening value based on the average deal value and is smeared by the deal value uncertainty. The other features of the salesperson are passed to the sales prospect and modelled by the deal.

3.3 Running the Model

A Monte-Carlo simulation is used to generate the data. Time is progressed forward month by month and at each time step every salesperson is tested to see if they generate any new deals. These deals are added to the pipeline. Old sale prospects in the pipeline are then progressed, each one is tested to see if it fails that month or if it completes. Simulating a few years of data can be done quickly to provide a baseline for the later modelling.

4 Modelling Historical Behaviour

There are some obvious defects with simulating historical sales data and then training a predictive model on it. The main issue is that the `natural/intuitive’ assumptions of modelling that one would go into the fitting the data also went into creating the data. This likely leads to better performance in the predictor than would be seen in a model based off real sales history. To minimize this effect, we will use simple techniques that do not make many assumptions.

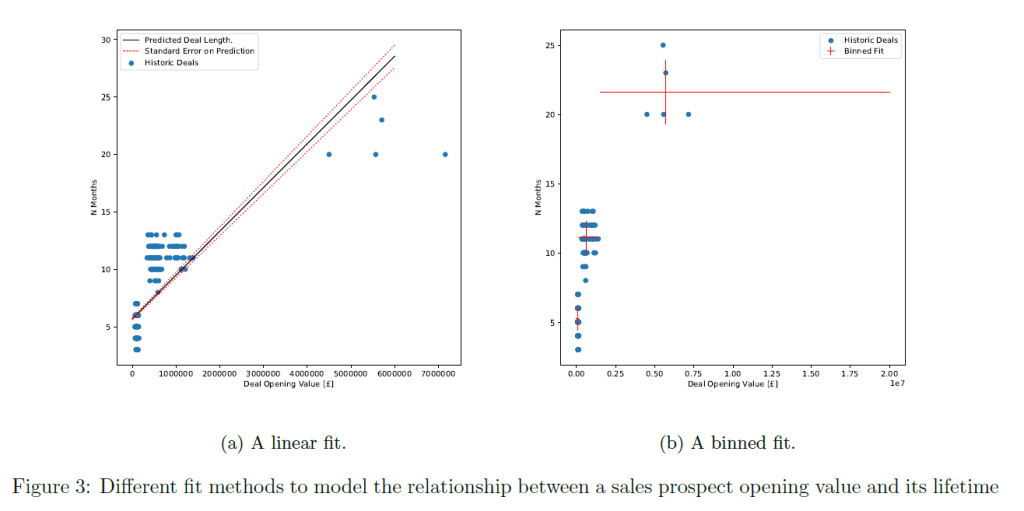

In predicting the future revenue from a sales pipeline, we need to know when a deal will close to realize the revenue. Figure 3 shows a sales prospect opening value versus its age upon completion and two methods to fit this data. A clear relationship between a sales prospect opening value and its lifetime can be seen. A linear model and binned fit both produce reasonable results for predicting an expected lifetime value. However, it can be seen the deals with a larger opening value are predicted to have a systematically longer lifetime than in the data. The linear model also under-predicts the variance. With real sales data it would be worth spending more time improving upon these models. However, as the training dataset is artificial the binned fit is good enough for the purposes of this research.

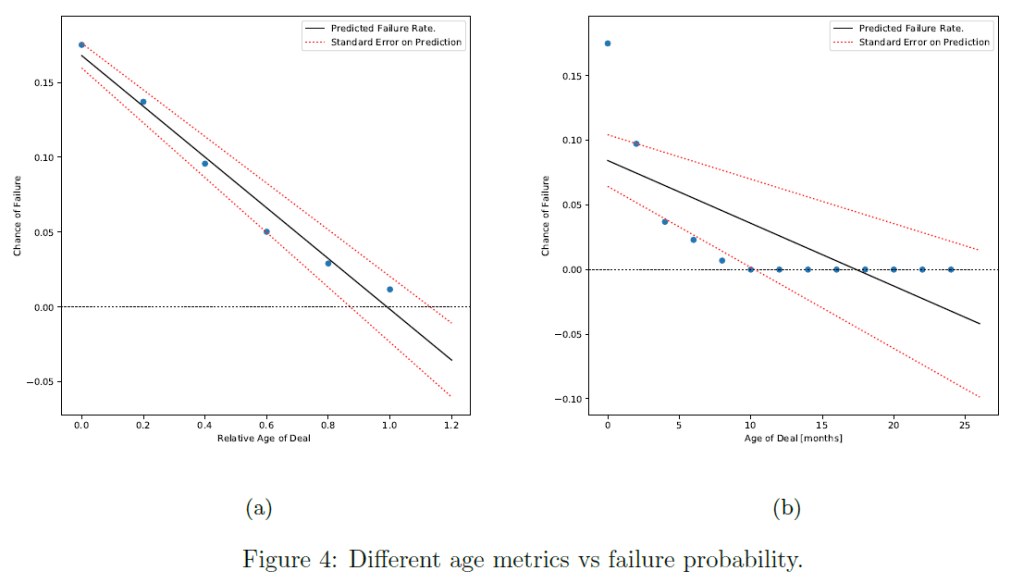

The next part of predicting a sales prospect eventual revenue is working out the chance it will fail before completion. The working theory is that deals have a similar chance of failing regardless of opening value. This is justified by assuming that salespeople who take on larger more complex deals are also better at completing them. Thus, the additional difficulty is balanced by the increased skill. Under this assumption, the primary determinant is the deals age. The older a deal the more hurdles it has overcome and the less it has in front of it. To determine the failure chance of a sales prospect the historical data is queried to check of those jobs which are of age x or older (i.e. were at age x at some point), what percentage failed. Figure 4 show the results of this query using the age of deals in months and the relative age of a deal compared to its age predicted by the binned lifetime fit model. A linear regression is fitted to both age metrics to generalize the results. The first thing to notice is that the linear model predicts negative failure chance probabilities. This is expected as the model has no concept of a maximum age and any negative relation will pass through zero at some point. It is corrected by enforcing a lower bound on the model prediction of 0. Looking at the failure rate verses the raw age raises two issues. The first is that the failure rate is clearly non-linear and the second is that the historical data shows a failure rate of 0 after 10 months. This is contrasted with a model based on relative age where a linear model describes the behaviour well and it gives a positive failure probability up until it is expected to complete. Due to this better behaviour, the relative age will be used a predictor of failure.

The final part of the modelling is the discount applied to the opening value when a deal closes. This is more straight forward than the other as it can be treated as a single number applied to all open deals. This is done by taking the average percentage discount applied to completed deals. The uncertainty on this value can be calculated by assuming it is normally distributed and taking its standard deviation.

5 Predicting the Future Value of A Pipeline

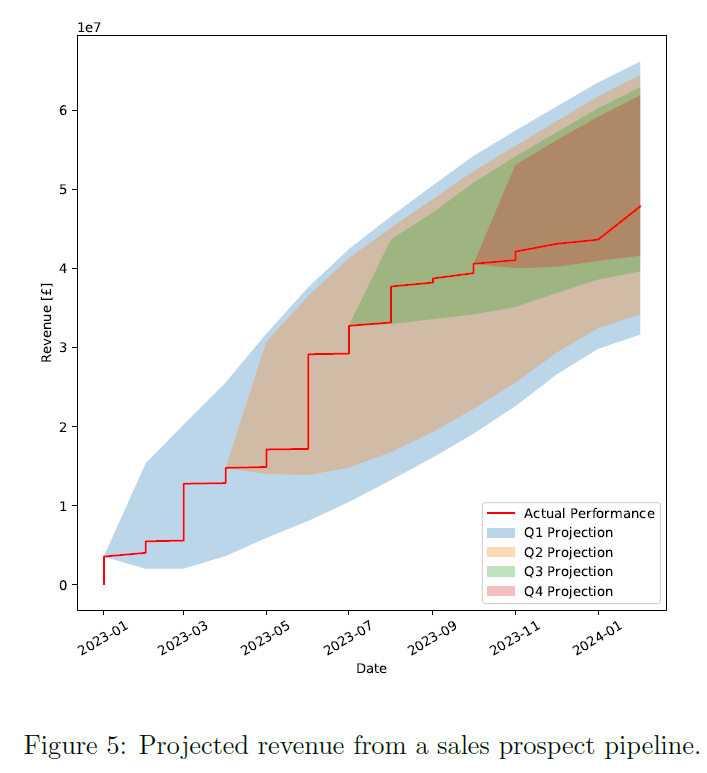

There is now enough information to evaluate the future value of a sales pipeline. For any given point in time a deal can be corrected by its expectation of completing, its chance of failing and the expected discount. With the assumptions stated in section 3 the uncertainty around this expected value can also be calculated. By applying the same process that was used to generate the historical data to the existing pipeline, it can be progressed through time to allow projections to be made each quarter and the `true’ revenue to be shown as well. Figure 5 shows a revenue projection with a 95% confidence of interval where the confidence interval implies that `real’ outcome will only have a 1 in 20 chance of going outside the bands. Although, the accuracy of the confidence intervals is only as good as the models used to derive it – so if there is a new situation not seen in the historical data then all bets are off.

A benefit of modelling the expected value of each deal at any point of time is it allows a sales manager to identify which sales and salespeople are most important for a given quarter to give them special attention. It also helps identify which salespeople are falling short of their targets to provide help.

6 Conclusion

The models used here are relatively simple and fall far short of those that would be needed to be useful in a real sales environment. There is bound to be all sorts of complex human behaviours that would need to be accounted for. However, as a proof of principle this research shows the practical application of modelling the sales life cycle. One area this research falls short on is modelling individual salespeople based on the historic data to produce predictions of revenue based on new sales prospects created throughout the year. With this, a sales manager could more accurately forecast their income and identify areas that need their attention. A more robust model could also help inform strategic decisions as their effect could be estimated and compared to their cost of implementation or opportunity cost.

Disclaimer: this article is not financial advice and should not be treated as such. It is a discussion based on personal circumstances and preferences and so should not be generalized to other situations without careful thought.

As shown in my previous post here, buying a property to rent out in Liverpool can be a good investment option. However, one property is not enough to retire on, so the next step is to see how this idea scales and evolves over time. The portfolio will be owned by a limited company to benefit from treating interest payments as tax deductible costs. While this is not the right choice for everyone, my own personal circumstances mean it is better for me. In my last article I looked at return-on-investment as the key metric to compare investments. However, my primary aim was to retire. This means extractable cash flow is a better metric to evaluate the success of a business venture as this can be used as a passive income stream. My goal is to have an income of around £3000 per month (pre-tax), but obviously the more the better.

This investigation will look into how the cash flow from a property portfolio evolves with time as more money is invested into the project. Three scenarios are considered.

That £20,000 can be invested into the company every six months for the first three years of the company which is used to purchase properties. Housing can be purchased only during the first three years.

That £40,000 can be invested into the company every six months for the first three years of the company which is used to purchase properties. Housing can be purchased only during the first three years.

That £40,000 can be invested into the company every six months for the first three years of the company which is used to purchase properties. Housing can be purchased during the first five years of the company.

1) Modelling the Business

In my previous post I used the price of £150,000 per house and a rental income of roughly £17,000 per year. While there are plenty of examples of properties with these numbers, to be conservative this model will assume each house costs £160,000 and rental income is £15,000. This is to account for the property market becoming more competitive with time either due to competition or our own market impact. Inflation will not be accounted for in this model as it is assumed income will scale with costs.

This model works by breaking the company down into four components, each representing a higher level of

abstraction: housing, management of the housing portfolio, the external funding and the investment decision

making part based on the input from the external funding and housing portfolio. Each house is treated as an

independent object with its own associated cost schedule and income which was described in my original blog post. The management piece takes collective action based on the cost schedule of its constituent houses. The external funding just adds money to the accounts that can be used to purchase more houses. The top level investment decision making part looks at the money available in the accounts to decide if the model has sufficient money to purchase another house.

An important part of this investigation is correctly modelling cash flow. In the original post we deducted the average cost of repairs each month to calculate the profit. In real life this money will need to sit somewhere and then be used to pay bills as they come up. If bills come close together then they may cost more than the company has saved. Equally, having multiple properties may mean there is enough income to cover bills on an ad-hoc basis and more money can be extracted from the company. This is discussed next.

Modelling of the Housing Portfolio

The housing portfolio part of the model is where the aggregated cash flow of all the houses is managed. It models the saving of money for maintenance and decides when to let money leave the housing portfolio to either be reinvested into more properties.

Any property is assumed to be in perfect condition after initial repairs are done at time of purchase. This assumption may be a generous one, but the conservative price the model assumes for the house smooths out this assumption.

After paying percentage based costs, such as property management fees, the rent is split into a part which can be extracted from the housing unit and one that is saved to cover future expenses. In the model there are two values considered when saving:

i) a minimum cash amount in the account to handle the maintenance costs and

ii) an additional amount of money stored per house as a contingency fund to make sure the company can always pay the bills.

Any money above the minimum cash amount is assumed to be stored in liquid assets yielding a 4% return. If the amount of money saved is equal to the desired saved amount than any additional income can be extracted from the housing portfolio. For example, if the portfolio has two houses, a minimum cash reserve of £10,000 and a per house reserve of £1,500, and the saved amount is £13,000, then any money that would be saved for future repairs above this amount can be extracted and re-invested. Repairs and maintenance are done according to the repair schedule described in the original article. Thus, every seven years after the house purchase a new kitchen will be bought for the property; estate agent fees will be paid every year. Costs associated with mortgages are paid every three years to remortgage the property. Money is first deducted from the cash reserve and then from the invested reserve. At the end of each month if the cash reserve is ever below the minimum amount money is transferred from the invested reserve if possible.

1.2 External Funding

This income stream represents invested money from the owners of the company. It assumes every six months an amount is invested into the company. In all scenarios investigated, this investment is assumed to carry on for three years to account for the investment horizon of this project.

1.3 Combined Business

The housing portfolio and external funding are treated as separate business units and every month the combined business extracts whatever money the business unit allows. The model will then purchase as many properties as allowed by its bank balance each month. Money extracted from the housing portfolio is taxed at a rate of 19% which is paid once a year in April. The company makes sure to keep enough money in reserve to pay tax. This reserve is an inefficient use of capital and can probably be improved. However, as the sums involved are small compared to the cost of a property this is likely to be a minor effect for this investigation.

2 Model Results

Before diving into the different business scenarios, it is worth looking at a single house again as some starting assumptions have changed since the last article. The cost of investing in a single property is £50,500 and the annual extractable income from it is £5,000. This works out to be a levered return of about 10% per annum. This is still a very promising starting point.

As described in the introduction, each scenario has different starting parameters. However, one common parameter across all scenarios is an initial bank balance of £35,000 so a house can be purchased after the first batch of external funding. Minimum cash and per house reserves are chosen such that the company does not go bankrupt over 30 years of projected maintenance. The business will be evaluated by its performance over the first 5 years with the assumption that it starts on 1st January 2020.

2.1 Scenario 1

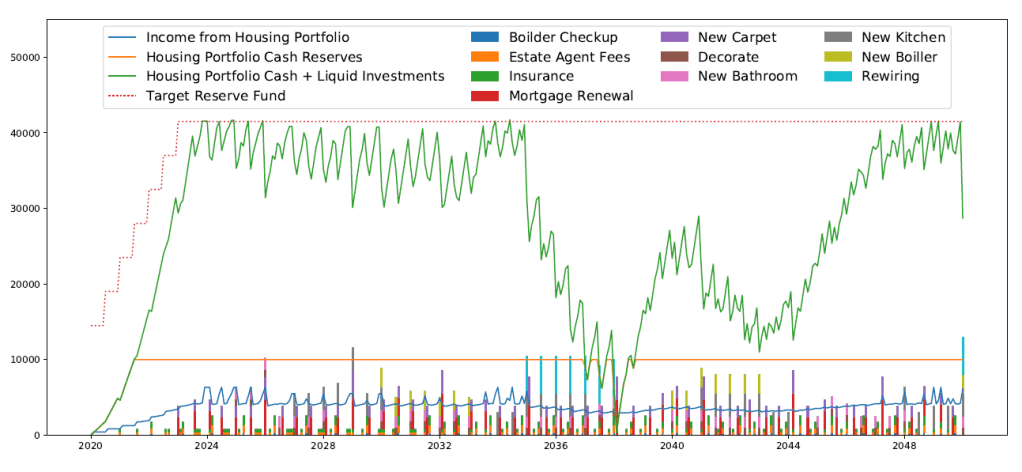

In scenario 1 £20,000 will be invested every six months for the first three years and houses are purchased for the first three years. The minimum cash reserve is £10,000 and the per house reserve is £3,500. Table 1 shows a summary of the business under scenario 1 for the first 5 years. Figure 1 shows a thirty year projection to give an idea of the full cash flow cycle. It can be seen that the reserve amount is driven by cash flow around 2035 when rewiring work is needed on the properties.

The average monthly income is derived from the cumulative income over the year divided by 12, so to smooth out any month-by-month fluctuations. These fluctuations are caused by the nature of the income stream. The rent component roughly stable, but cash can be extracted when the saving target has already reached and from returns on the invested fraction of the cash reserve. A large bill can reduce the saved reserve enough that it takes months to recover and hence the extractable money is reduced. An important point under this scenario is that cash from the invested reserve and not saving above our reserve amount contributes a significant amount to total cashflow. In year 5 the average income from 3 houses purely from rent is around £1,200 but the average income is £2,000.

Table 1: Summary of the business under scenario 1.

Year

Average Monthly Income [£]

Number of Houses

2020

400

1

2021

600

2

2022

1100

3

2023

1500

3

2024

2000

3

Figure 1: 30 year projection of business cash flow for scenario 1.

2.2 Scenario 2

In scenario 2 £40,000 will be invested every six months for the first three years and houses are purchased for the first three years. The minimum cash reserve is £10,000 and the reserve per house is £4,000. Table 2 shows a summary of the business under scenario 2 for the first 5 years. Figure 2 shows a thirty year projection to give an idea of the full cash flow cycle. Doubling the investment results in more than doubling the monthly income. This is because the portfolio starts to generate enough money on its own to purchase new properties. However, the external investment still dominates the available income for the business over the period that is being looked at.

Table 2: Summary of the business under scenario 2.

Year

Average Monthly Income [£]

Number of Houses

2020

560

2

2021

1500

4

2022

2800

6

2023

4200

7

2024

5200

7

Figure 2: A 30 year projection of cash flow in Scenario 2

2.3 Scenario 3

In scenario 3 £40,000 will be invested every six months for the first three years and houses are purchased for the first five years. In this scenario, the minimum cash reserve is £10,000 and the reserve per house is £2,000. Table 3 shows a summary of the business under scenario 3 for the first 6 years. Figure 3 shows a thirty year projection to give an idea of the full cash ow cycle. The per house reserve value is lower than in scenario 1 and 2 as the monthly maintenance contribution from the larger number of houses can offset more of the repair costs. Despite having more houses, the monthly income after 5 years does not increase by much. This is because in scenario 2 money could be returned to investors when the saving threshold was met around 2023. In scenario 3 the saving threshold is not met until after 2024.

Table 3: Summary of the business under scenario 3

Year

Average Monthly Income [£]

Number of Houses

2020

550

2

2021

1450

4

2022

3400

6

2023

4300

8

2024

5250

9

2025

5550

9

Figure 3: A 30 year projection of cash flow under scenario 3.

3 Summary

Our current models suggest that the idea of purchasing houses to produce a stable income is a viable one. However, only scenario 2 and 3 produce an income which a single investor could live. The similar income in scenario 2 and 3 suggest scenario 2 is the minimum viable scenario to meet my aim of retiring early and will also let me do so the quickest. However, waiting two more years before stopping reinvestment would allow the company to function on a much lower reserve amount and the higher number of houses in model means the stable rent component of the income stream will be larger.

One area this model does not cover is the effect of interest rate changes. It assumes a low interest regime at least for the next 5 years. Any increase to interest rates would reduce the profitability of this project as cash would need to be directed to pay off debt and to cover increased costs of servicing the existing debt.

Is a Buy-to-Let Residential Property a Good Investment?

Disclaimer: this article is not financial advice and should not be treated as such. It is a discussion based on personal circumstances and preferences and so should not be generalized to other situations without careful thought.

Like many people I have often dreamed of having a passive income stream and living my life on a beach somewhere. One of the more common recommendations to achieve this is to invest your money into a property which you can then rent out to other people. This is a tried and tested method but is it better than other forms of investment? Two answer this question, I need to answer two smaller questions:

How to compare two investments.

How to evaluate a house with respect to this metric.

The first question is easier to answer but more subjective. A variety of factors may affect what you consider a good investment. For my aim of having a passive income, at least one of them is that minimal effort is required in maintaining the investment. Given this constraint we are left with a smaller subset of available investments. There are also a host of other constraints most people will apply such as tax considerations and tolerance of risk but this is an article about numbers, not about financial planning, so I will leave it to the reader to consider those issues for themselves. Of the remaining investment opportunities, I will use return-on-investment (RoI) as the metric of quality to compare investments. The RoI is determined by the annual return divided by the cost of the investment. Now that question i) is answered, evaluating a house as an investment with respect to my chosen metric should be more objective. The bulk of this article discusses how to determine a buy-to-let property’s RoI.

1) First Approximation

The first approximation of the RoI of buy-to-let property is to sum the annual rental income of the property with the change in house value and then divide by the cost of the house. For this article, change in house value is ignored as the business model is not one of housing development and owners have little control over broader trends in the housing market.

For the purposes of this article, I will assume I am looking at student housing in the Kensington area of Liverpool. This choice is based upon previous research looking at housing prices and rental income in large cities on Zoopla, but it is not discussed as it will most likely form another blog. In this area a 4-bedroom house can be purchased for £150,000 and each room can be rented for £355 per calendar month (pcm). This works out to be an annual income of about £17,000. Thus, the naïve asset-level RoI on this property is 11.3%. This is a good return compared to the average annual return on stocks of about 7% over the last few decades (7.19% for the S&P 500 over the last 20 years and 6.4% of the FTSE 100 over the last 25 years). Stocks returns are just used as a benchmark and have other benefits such as tax treatment and involving little work after picking them which I will not discuss here.

This obviously is not the whole story. Anyone who has owned a property will quickly point out that there are a lot of costs associated with running a property, which mean that the nominal annual rental income can quickly be reduced. Equally, anyone who has invested in properties before will point out that you can reduce upfront capital by borrowing money. In our example, this means getting a mortgage. Thus, the actual equity return on investment is based upon the original cashdeposit plus any transaction costs incurred, such as stamp duty and lawyer fees. Evaluating these two factors will be essential to figuring out the RoI of our target buy-to-let property.

2) Cost of a Property

Buying a property involves interacting with a lot of different people and each person is liable to charge for the privilege. Table 1 provides a list of the key costs and an estimate of their cumulative value assuming a property is bought for £150,000 in the UK. The largest single cost when buying a property is the deposit. For a buy-to-let property in a reasonable condition the minimum deposit is around 25% of total property value. The second largest cost is the stamp duty which is the tax charged by the government on the transaction. This is a tiered tax that depends on the property value, but the main component is the 3% surcharge added when the buyer already owns a property. In total, we estimate that it costs us £47,450 in upfront cash to purchase our target property. The cost estimates described here are based on experience in buying past property.

Table 1: Illustrative costs associated with purchasing a buy-to-let property.

Cost Item

Amount [£]

Deposit

37,500

Stamp Duty

5,000

Lawyer

1,000

Surveyor

600

Repairs

1,000

Mortgage Costs

2,350

Total

47,450

3) Income from a Property

From our first approximation we already know the gross monthly income of our property, £1,420 pcm (assuming full occupancy). The important part is working out all the ongoing costs associated with renting a property, which can be split into three key areas.

Maintenance costs – these are the costs associated with keeping the property up to date, insurance and repairing any damage done by tenants.

Mortgage costs – these are the costs associated with servicing our debt on the property such as the monthly repayments on interest as well as the costs of renegotiating a new mortgage every few years.

Percentage based costs – these are the costs of doing business such as hiring a property manager and accounting for any periods where the property is not let out which are best expressed as a percentage of the rent.

For easier comparison with the monthly gross income these costs are also calculated as monthly figures.

3.1) Maintenance Costs

Inside a house there are many things that need to be updated at regular intervals to keep the property in a fit state for tenants. It has been assumed that emergency repairs can be covered via insurance and damage done by tenants in a non-emergency manner will be covered by security deposits. This leaves update/replacement costs to be modelled. Table 2 breaks down the individual costs to provide as comprehensive a model as possible. For each cost I have provided a total cost estimate, a time between renewal cost and the resulting monthly cost. It is worth pointing out that these are best guesses on the actual costs and so have round values. With this caveat in mind, I estimate the monthly cost associated with maintenance and repairs to be £240.

Table 2: List of maintenance costs and update frequencies.

Item

Cost [£]

Years Between Update

Cost Per Month [£]

New Kitchen

3,000

7

35.71

New Bathroom

1,500

5

25.00

New Boiler

2,500

10

20.83

Boiler Checkup

100

1

8.33

Decorator

1,000

4

16.67

Estate Agent Fees

350

1

29.17

Electrical Rewiring

5,000

15

27.78

Insurance

410

1

34.17

New Carpet

1,500

3

41.67

Total

239.33

3.2 Mortgage Costs

The interest charged on an interest-only 75% loan-to-value (25% deposit) mortgage with a three-year fixed rate is about 3% (as of February 2020). This works out to be about £280pcm in interest payments. In addition to these interest payments banks typically also charge an upfront fee of £2,000 every time a mortgage is renewed and a mortgage broker will charge around £350 to find a new mortgage. Including these extra costs with the interest fees results in a monthly mortgage cost of £345.

3.3 On-going costs

In addition to the mortgage and maintenance there are on-going costs which are best expressed as a percentage of the rental income. There are two main line items here. The first is the cost of a property manager. As the properties will be in Liverpool it would be impractical to not have a property manager. Property managing services typically take a cut of the rental income and 10% is representative. A harder cost to model is not having tenants in the property (void periods) and so no rental income coming in. To make it easier to model, it is assumed one month a year is void and this loss is treated as a reduction in rent across all months. This works out to be the monthly rental income being reduced by 8%. Combined this means 18% of the rental income is lost before it ever hits our bank account which costs about £255 per month.

3.4 Summary of costs and incomes.

A summary of the costs and income can be seen in Table 3. It shows that per month £570 of the rental income can be treated as profit while the rest should be saved to pay for future costs. This roughly means that there is a 40% profit margin on the property which is a good amount of fat to have if some of the assumptions about costs are wrong. A £570pcm profit equates to an annual income of £6,840.

Table 3: Summary of property cash flow.

Description

Cash Flow [£]

Rental Income

1,420

On-going Costs

(255)

Mortgage costs

(345)

Maintenance Costs

(240)

Total

570

4. Conclusion

Section 2 calculates that the equity cost of the assumed property is £47,450 and in section 3 the annual income is worked out to be £6,840. This gives a levered return-on-investment of 14.4%. This is almost twice that of investing in stocks. It is worth pointing out that this investigation does miss some important aspects. First, it looks at a property in isolation and does not consider the personal costs (e.g. time commitments) associated with running this property. It also ignores interest rate risk. We are in a period of unusually low interest rates and the profit from this venture would be eaten up quickly should they increase. Even with these caveats, this study covers enough of the key elements to suggest that purchasing a property is worth looking into more.